What Is a Tax-Free Savings Account (TFSA) in Canada? A Complete Guide

The Tax-Free Savings Account, commonly called a TFSA, is one of the most powerful financial tools available to Canadians. Since its introduction by the federal government in 2009, it has helped millions of Canadians grow their savings completely tax-free.

This guide explains exactly what a TFSA is, how it works, what you can hold inside one, and how to make the most of it.

What Is a TFSA?

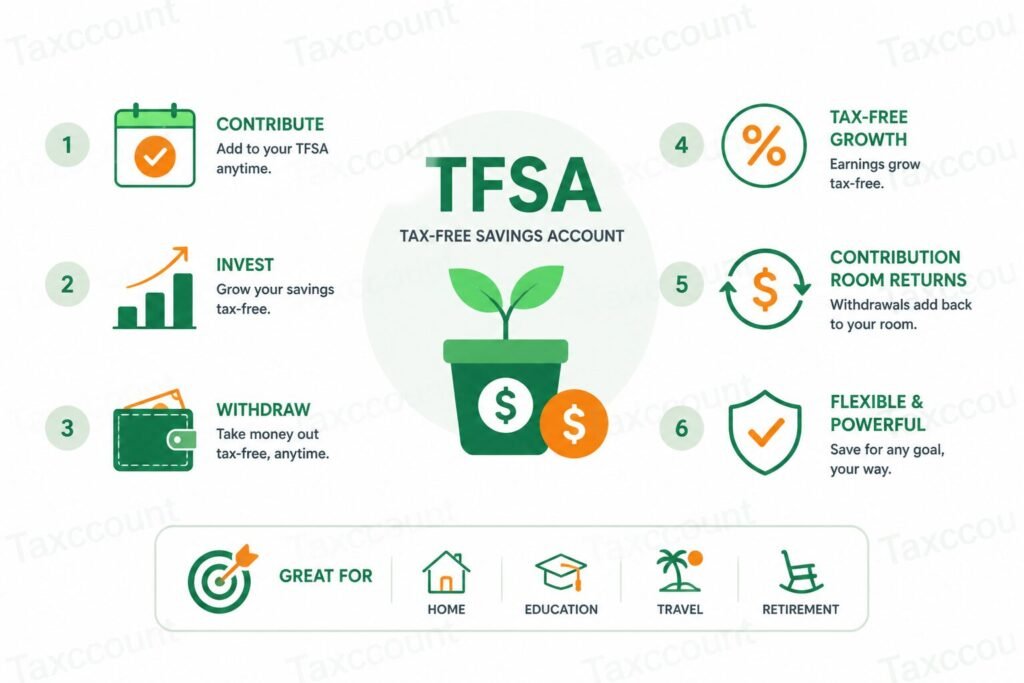

A TFSA is a registered account available to all Canadian residents aged 18 or older who have a valid Social Insurance Number (SIN). The key benefit is that any money you earn inside a TFSA — whether interest, dividends, or capital gains — is completely tax-free. You also do not pay tax when you withdraw the money.

Maximize Your TFSA

☎️ Get HelpWho Can Open a TFSA?

You are eligible to open a TFSA if you:

- Are a Canadian resident

- Are 18 years of age or older

- Have a valid Social Insurance Number (SIN)

Non-residents can technically hold a TFSA, but contributions made while non-resident are subject to a 1% monthly tax, so it is generally not recommended.

How Much Can You Contribute to a TFSA?

Each year, the federal government sets an annual TFSA contribution limit. Your total available room accumulates from the year you turned 18 and became a resident of Canada — even if you have never opened a TFSA.

Key points about TFSA contribution room:

- Contribution room carries forward indefinitely if unused

- When you withdraw from your TFSA, that amount is added back to your contribution room at the start of the next calendar year

- Over-contributing results in a 1% monthly penalty tax on the excess amount

- To check your exact available room, log in to CRA My Account

What Can You Hold Inside a TFSA?

A TFSA is not just a savings account. You can hold a wide variety of investments inside one:

- Cash and high-interest savings

- GICs (Guaranteed Investment Certificates)

- Mutual funds

- Exchange-traded funds (ETFs)

- Stocks and bonds

- Certain types of securities listed on designated stock exchanges

How Does a TFSA Differ from an RRSP?

Both TFSAs and RRSPs are registered accounts with tax advantages, but they work differently:

| Feature | TFSA | RRSP |

|---|---|---|

| Contributions | Not tax-deductible | Tax-deductible |

| Growth | Tax-free | Tax-deferred |

| Withdrawals | Tax-free | Taxed as income |

| Contribution room on withdrawal | Restored next year | Not restored |

| Best for | Any savings goal | Retirement savings |

Can You Withdraw from a TFSA at Any Time?

Yes. You can withdraw any amount from your TFSA at any time for any reason without paying tax on it. There are no restrictions on when or how much you can withdraw. The withdrawn amount is added back to your contribution room at the start of the next calendar year.

What Happens to a TFSA When You Die?

If you name your spouse or common-law partner as a successor holder, they can take over your TFSA without affecting their own contribution room. If you name any other person (such as a child) as a beneficiary, the TFSA’s value at the time of death passes to them tax-free, but any growth after death is taxable.

Maximize Your TFSA with Taxccount

Using your TFSA effectively is one of the smartest financial moves a Canadian can make. Taxccount helps individuals and families understand how to optimize their registered accounts — including TFSAs, RRSPs, and FHSAs — as part of a complete tax strategy.

Book a free consultation with Taxccount today and let our Canadian tax experts help you keep more of your money.

Table of Summary

Here is the blog information in 6 easy rows for quick understanding:

| Section | Easy Information |

|---|---|

| 1. Topic | The blog explains Tax-Free Savings Accounts (TFSAs) in Canada and how they work. |

| 2. What Is a TFSA | A registered account for Canadians 18+ with a valid SIN. Earnings (interest, dividends, capital gains) are tax-free, and withdrawals are also tax-free. |

| 3. Contribution Rules | Annual contribution limits are set by the federal government. Contribution room carries forward indefinitely; withdrawn amounts are added back next year; over-contributions incur a 1% monthly penalty. |

| 4. Eligible Investments | TFSAs can hold cash, GICs, mutual funds, ETFs, stocks, bonds, and certain securities. |

| 5. TFSA vs RRSP | TFSA contributions are not tax-deductible, growth is tax-free, withdrawals are tax-free, and contribution room is restored on withdrawal. RRSP contributions are tax-deductible, growth is tax-deferred, withdrawals are taxed, and room is not restored. |

| 6. Death & Successors | Naming a spouse/common-law partner as successor allows them to inherit the TFSA tax-free. Other beneficiaries receive the value at death tax-free, but subsequent growth is taxable. |

Frequently Asked Questions

Is a TFSA better than an RRSP?

It depends on your income and goals. A TFSA is generally better for flexible savings and lower-income earners. An RRSP is better for reducing taxable income today and saving for retirement. Many Canadians benefit from using both.

Do TFSA earnings need to be reported to CRA?

No. Income earned inside a TFSA does not need to be reported on your tax return and does not affect your taxable income or benefits.

Can I have more than one TFSA?

Yes. You can hold multiple TFSAs at different institutions, but your total contributions across all TFSAs cannot exceed your available contribution room.

What happens if I over-contribute to my TFSA?

CRA will charge a penalty tax of 1% per month on the excess amount until it is removed. Monitor your contributions carefully using CRA My Account.

Grow Tax-Free Savings

☎️ Get HelpThis is general information only and not professional advice. Consult a professional before acting.