Do You Pay Tax on Inheritance in Canada? What You Need to Know

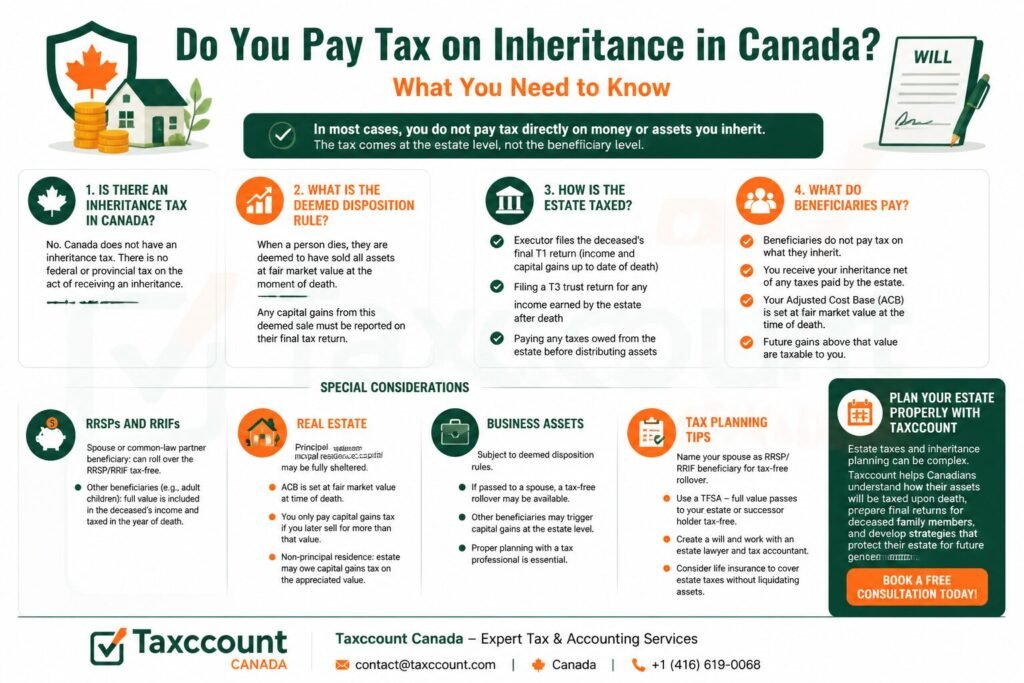

One of the most common questions Canadians ask when receiving an inheritance is whether they will owe tax on it. The short answer is: in most cases, you do not pay tax directly on money or assets you inherit. But this does not mean inheritance is completely tax-free. The tax comes at the estate level, not the beneficiary level.

This guide explains how inheritance is taxed in Canada, what the deemed disposition rule means, and what you need to know if you are receiving or leaving an inheritance.

Is There an Inheritance Tax in Canada?

No. Canada does not have an inheritance tax. There is no federal or provincial tax specifically on the act of receiving an inheritance. Unlike the United States, which has estate taxes at the federal level and in some states, Canada eliminated its federal estate tax decades ago.

However, the estate of the deceased person may be subject to income tax before assets are distributed to beneficiaries.

Plan Your Estate Today

☎️ Get HelpWhat Is the Deemed Disposition Rule?

When a person dies in Canada, the Income Tax Act treats them as having sold all of their assets at fair market value at the moment of death. This is called the deemed disposition rule.

Any capital gains triggered by this deemed sale must be reported on the deceased person’s final tax return. The estate pays the resulting tax before distributing assets to beneficiaries.

How Is the Estate Taxed?

The executor of the estate is responsible for:

- Filing the deceased’s final T1 income tax return (reporting all income and capital gains up to the date of death)

- Filing a T3 trust return for any income earned by the estate after death

- Paying any taxes owed from the estate before distributing assets to beneficiaries

What Do Beneficiaries Pay?

As a beneficiary, you generally do not pay income tax on amounts you inherit. You receive the inheritance net of any taxes already paid by the estate. However, your adjusted cost base (ACB) for inherited assets is set at fair market value at the time of death — meaning any future gains you realize above that value will be taxable to you.

Inheriting an RRSP or RRIF

RRSPs and RRIFs are treated differently:

- If you are the surviving spouse or common-law partner named as beneficiary, the RRSP or RRIF can be rolled over into your plan without immediate tax

- If you are any other beneficiary (such as an adult child), the full value of the RRSP/RRIF is included in the deceased’s income in the year of death and taxed accordingly on their final return

Inheriting Real Estate

If the property was the deceased’s principal residence, the capital gain may be fully sheltered by the principal residence exemption. When you inherit the property:

- Your ACB is set at the fair market value at the time of death

- You only pay capital gains tax if you later sell for more than that inherited value

- If it was not the principal residence, the estate may owe capital gains tax on the appreciated value

Inheriting a Business

Business assets are also subject to deemed disposition rules. If a family business is passed to a spouse, a tax-free rollover may be available. Other beneficiaries may trigger capital gains at the estate level. Proper estate planning with a tax professional is essential in these situations.

Tax Planning for Inheritance

To minimize the tax burden on your estate and beneficiaries, consider:

- Naming your spouse as RRSP/RRIF beneficiary for a tax-free rollover

- Using a TFSA — the full value passes to your estate or successor holder tax-free

- Creating a will and working with an estate lawyer and tax accountant

- Considering life insurance to cover estate taxes without liquidating assets

Plan Your Estate Properly with Taxccount

Estate taxes and inheritance planning can be complex. Taxccount helps Canadians understand how their assets will be taxed upon death, prepare final returns for deceased family members, and develop strategies that protect their estate for future generations.

Book a free consultation with Taxccount today and make sure your estate is structured as tax-efficiently as possible.

Table of Summary

Here is the blog information in 6 easy rows for quick understanding:

| Section | Easy Information |

|---|---|

| 1. Topic | The blog explains inheritance taxation in Canada and how it affects estates and beneficiaries. |

| 2. Inheritance Tax | Canada does not have an inheritance tax; beneficiaries generally do not pay tax on money or assets received. |

| 3. Deemed Disposition Rule | Upon death, the estate is treated as having sold all assets at fair market value; capital gains are reported on the deceased’s final tax return. |

| 4. Estate Responsibilities | The executor files the deceased’s final T1 return, files T3 for income after death, and pays any taxes before distributing assets. |

| 5. Beneficiary Rules | Beneficiaries receive inheritance net of taxes already paid. Future gains above the fair market value at death are taxable. RRSP/RRIF, real estate, and business inheritances have specific rules. |

| 6. Tax Planning | Strategies include naming a spouse as RRSP/RRIF beneficiary, using TFSAs, creating a will, and considering life insurance to cover estate taxes. Proper planning reduces tax burden for heirs. |

Frequently Asked Questions

Do I pay income tax when I receive an inheritance in Canada?

Generally no. Beneficiaries do not pay income tax on inherited money or assets. The estate pays any applicable taxes before distribution.

What is the deemed disposition rule in Canada?

It is a CRA rule that treats a person as having sold all their assets at fair market value at the moment of death. This may trigger capital gains that are taxable on the deceased’s final return.

Do I pay tax on an inherited RRSP?

If you are the surviving spouse, the RRSP can roll over tax-free. For other beneficiaries, the full RRSP value is included in the deceased’s income and taxed on their final return.

Are inherited investments taxable in Canada?

The estate may owe capital gains on investments at the time of death. As a beneficiary, you inherit at the fair market value at death, so you only pay tax on gains you realize after that point.

Protect Inherited Assets

☎️ Get HelpThis is general information only and not professional advice. Consult a professional before acting.